Don't miss the chance to work with top 1% of developers.

Sign Up Now and Get FREE CTO-level Consultation.

Confused about your business model?

Request a FREE Business Plan.

How to Successfully Implement Blockchain Into Business

Table of contents

Blockchain technology has taken the business world by storm. There is no second opinion that this technology is going to stay here for a long time. This is the reason why most businesses from around the globe want to implement blockchain into their business.

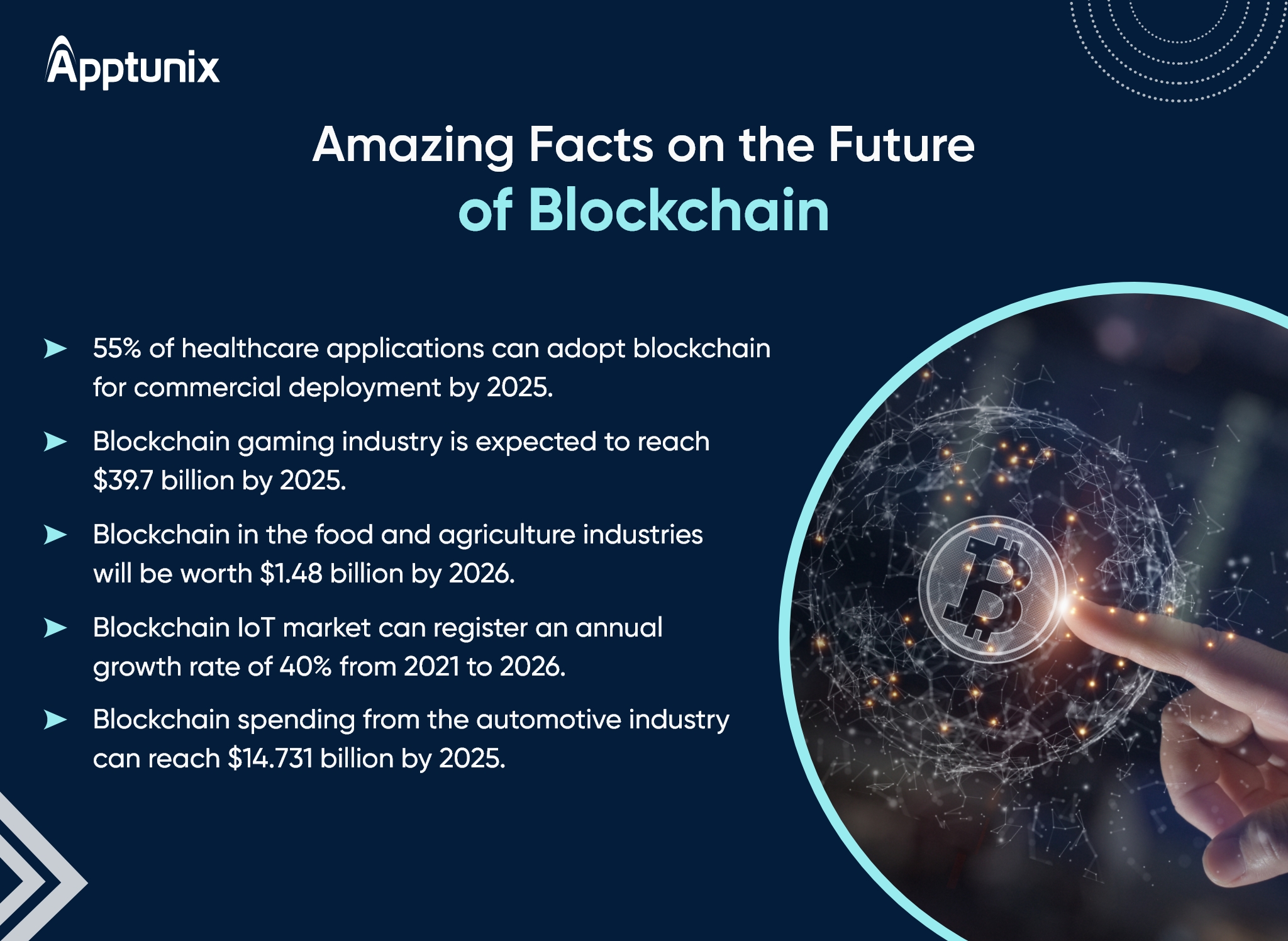

And why not so when this distributed encrypted database model has a high potential to solve online trust and security-related problems? Even the statistics speak on its behalf. According to a recent survey, the compound annual growth rate of 56.3% is going to make the blockchain industry worth $163.83 billion by 2029.

So if you are planning to set up blockchain in your business it’s the right time to dive in. But blockchain implementation is not as easy as it seems to be. To make it easy for you this guide offers everything you must know about integrating blockchain technology into your business.

So let’s begin the journey without any delay.

Benefits of Implementing Blockchain Technology Into Business

You might be wondering whether it’s a wise decision to go with blockchain or not. Well, blockchain technology has a lot to offer. It has become one of the key technologies to drive business transformation. Some of its major advantages are

- Transparency: Blockchain has emerged as a perfect solution to transparency that centralized systems have blocked. Blockchain operates through a decentralized network where validation takes place through consensus. It means every node can keep a copy of the transaction ensuring transparency. Apart from this, the automatic updates ensure instant and transparent transactions.

- Security: Blockchain is immutable. It means once the data is written it can’t be reverted. This technology encompasses encryption to prevent any breach. There is a hashing that connects the new transaction with the previous transaction to provide enhanced security.

Apart from this, the transaction copy held by each node can’t be changed by hackers. This will increase the trust as well as the integrity of the system. - Decentralization: This is the prime benefit of going with blockchain where a distributed network handles supervision and decision-making. It further benefits through the removal of intermediaries, speeding up operations, and lowering operational costs.

- Tokenization: Blockchain deals with Tokens. The good thing about asset-based tokens is, they can be defined as digital claims on a physical asset. Whether it’s crude oil, gold, real estate, equity, art, cars for rentals, legal documents, or any other physical assets all can be tokenized and used in one’s favor.

Moreover, once the tokenization is over, you can store the asset digitally. This is when you can trade it or sell it anytime anywhere.

Also Read: How Is Blockchain Technology Revolutionizing Mobile Apps?

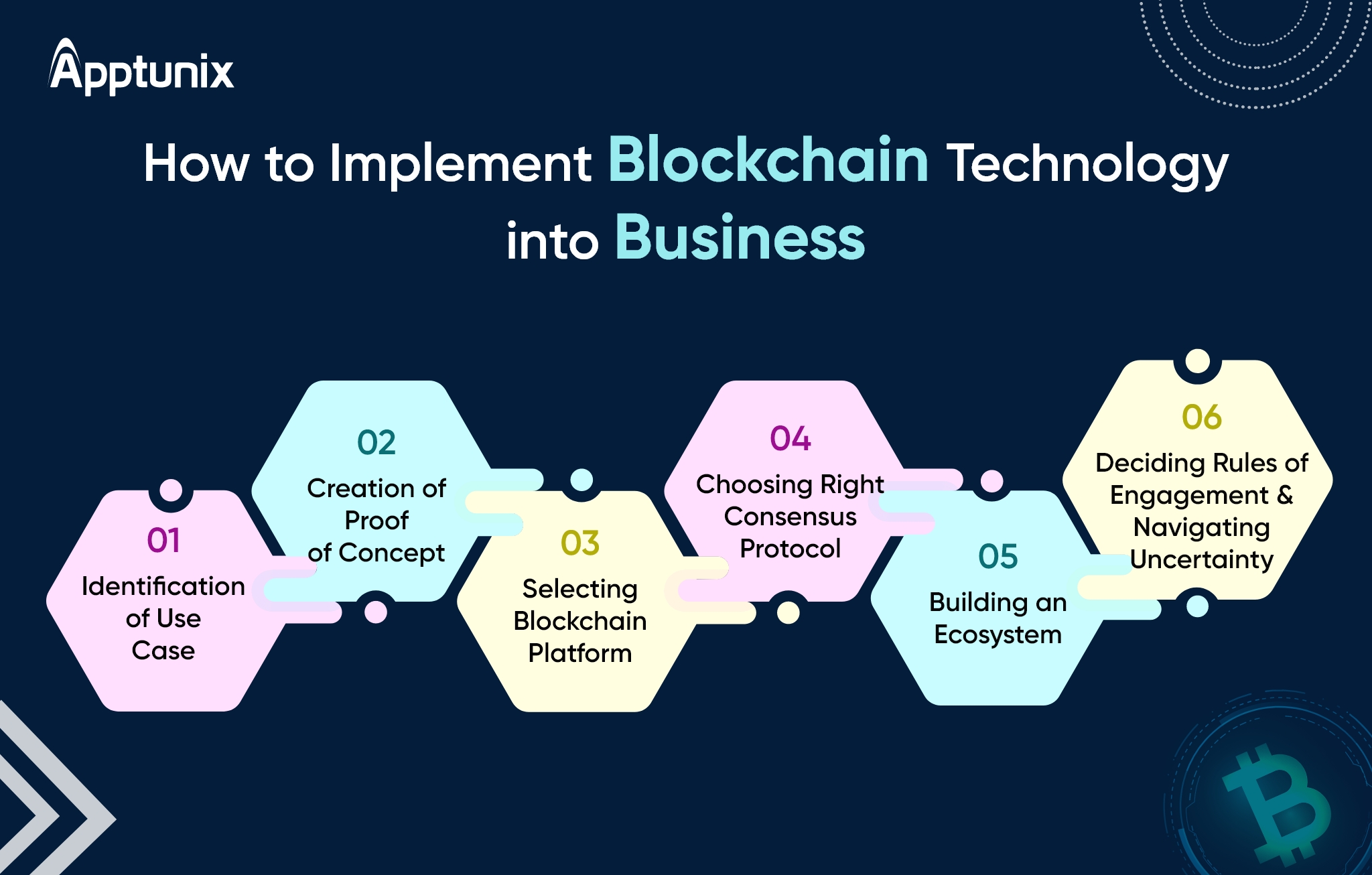

6 Steps to Implement Blockchain Successfully

Blockchain implementation needs a complete strategy. You are required to consider both the current situation as well as the future plans before making a move. To make it easy, here is a complete step-by-step process to implement blockchain successfully.

Step 1: Identification of Use Case

It is essential to identify, clarify and organize your business needs. You must be clear about the problems in hand that you want to solve via blockchain. The best way is, to go with the pilot project, analyze the outcomings, and then proceed further. It is good to ask yourself questions like

- What is the impact of blockchain technology on the current market?

- How does blockchain help my business?

- Can blockchain technology solve my business problem?

- How does blockchain reduce cost?

- Is blockchain technology suitable for my business in the long run?

- How does blockchain improve customer service?

Step 2: Creation of Proof of Concept

Once the use case is identified, it is necessary to make a valid proof of concept (PoC). PoC is a strategic procedure used for the evaluation of blockchain feasibility for the business. All you need to do is to understand the planning phase and evaluate the steps. Let’s go through some steps to create a PoC.

- Develop a complete set of guidelines for explaining the business project.

- Make a prototype to involve design, code, and sketches.

- Test the prototype to know the business happenings.

- Thoroughly analyze the Minimum Viable Product (MVP) for incorporating top features.

Step 3: Selecting Blockchain Platform

It is crucial to carefully choose the blockchain platform. You must be aware of the technology that suits your business. It is good to ascertain whether the technical team is organized and equipped with an open-source station. Apart from this, budget, the general level of understanding, etc are some of the factors you can consider while choosing the platform. To help you with the same, here are some of the popular blockchain development platforms:

- Ethereum

It is basically used for building innovative contracts. A reason why it is being used by several organizations for determining the potential scaling rate. Ethereum is one of the best options for businesses that want to build apps capable of running on blockchain-like software. - Hyperledger Fabric

This platform is basically used for building creative private blockchain apps. A Hyperledger expert can develop technical solutions that build organizations through the implementation of blockchain in an app. - Stellar

This platform supports a distributed exchange mode that allows users to easily send payments in specific currencies. This is due to the fact that the network automatically performs the forex conversion. - Quorum

The good thing about Quorum is, it eliminates data tampering in business transactions. This allows organizations to make secure transactions while maintaining privacy. - Multichain

As indicated by its name itself this platform can be employed in various industries. It doesn’t matter whether it’s the healthcare sector, education sector, banking & finance sector, eCommerce sector, or so on Multichain is a good option to go with. - OpenChain

If you are looking forward to maximizing every aspect of your business’s Human Resource Management (HRM), OpenChain is one of the best options to go with.Also Read: Top 5 Blockchain Development Platforms to Build Robust Applications

Step 4: Choosing Right Consensus Protocol

When it comes to a distributed network, consensus protocol alone is capable of creating an indisputable system of agreement between the devices. Some of these protocols are

- Proof of Work (PoW)

PoW counters cyber attacks like DDoS. it also validates transactions to create new blocks. - Proof of Stake (PoS)

A combination of random qualifications like age, wealth, performance, etc are taken into account to select a developer for a subsequent block. - Delegated Proof of Stake

It ensures approvals of transactions as there is an involvement of a fixed set of miners in the activities. - Byzantine Fault Tolerance (BFT)

There can be a time when the network components are unresponsive. In this scenario, BFT helps achieve consensus by depending on the same value. - Proof of Weight (PoW)

It helps achieve agreement by depending on the weight of the cryptocurrency the miner has.

Step 5: Building an Ecosystem

Blockchain technology functions best with the participation of stakeholders. So you are required to build an industry ecosystem, a community within the organization that can understand the technology’s potential and helps to improve standards & rules.

Stakeholders can decide the rules, decide the right control framework, ensure costs & benefits, affirm governance mechanisms and validate various other blockchain functionalities. To make it easy for you, here are steps to build a solid ecosystem.

- Begin with Smaller Ecosystems

It is good to build a blockchain with few stakeholders who are capable of expanding it later. - Search for a Community

Widen your network via blockchain consortia and consider more industry apps. - Conduct a Competitive Analysis

Analyze your market competitors and look for potential partners. - Use Robust Governance for Standardizing Data

Build standard naming conventions and system-wide data models.

Step 6: Deciding Rules of Engagement & Navigating Uncertainty

The new ecosystem must carry the ability to solve the organization’s issues. It must also address the privacy implications, compliances, and cybersecurity issues. Make sure that your business must comply with the emerging blockchain policies and best practices. Here is the key plan to help you out on the same.

- Risk Confrontation

It is beneficial to involve compliance, cybersecurity, and legal team in the blockchain development team for confronting risk. - Evaluate Privacy Implications

Needless to say, data is a crucial feature of blockchain. So it is good to invest in data processes while making sure it is fitting into privacy strategies like General Data Protection Regulation (GDPR). - Utilize Current Regulations

You can apply current regulations in various ways to stay agile. - Observe Evolving Regulations

It is good to involve regulators in order to tackle the laws pertaining to data usage and protection that keep on changing on a timely basis.

4 Things to Consider While Implementing Blockchain Technology

Implementing blockchain technology into business has its own challenges. So you must be aware of certain things that must be considered while implementing this technology.

- Rigorous Testing

To make sure your system actually works, you are required to test it fully. You can first test it in a controlled setting, then in a real working environment. It is possible that you may find a unique variable that hasn’t been considered previously. This can really hamper blockchain implementation results. - A Room for Failure

You must understand that every aspect of your blockchain implementation protocol is not going to work the way you desired. So the best way to tackle this situation is to make a copy of all issues and failures and then fix them later using different methods. You can also go with trial and error to get the results you want. - Focus is the Key

It is crucial to keep your initial target in mind while making edits and improvements in the protocol. You must focus on making the system more effective for users and not on changing it completely to make it workable. - Prepare for the Future

Once you have successfully created a workable blockchain implementation protocol you must start preparing yourself for the next challenge. Observe the protocol at hand to see how you can further improve it. Make sure the blockchain is scalable.

# Interesting Fact: 88% of senior executives worldwide think that blockchain technology is soon going to achieve mainstream adoption.

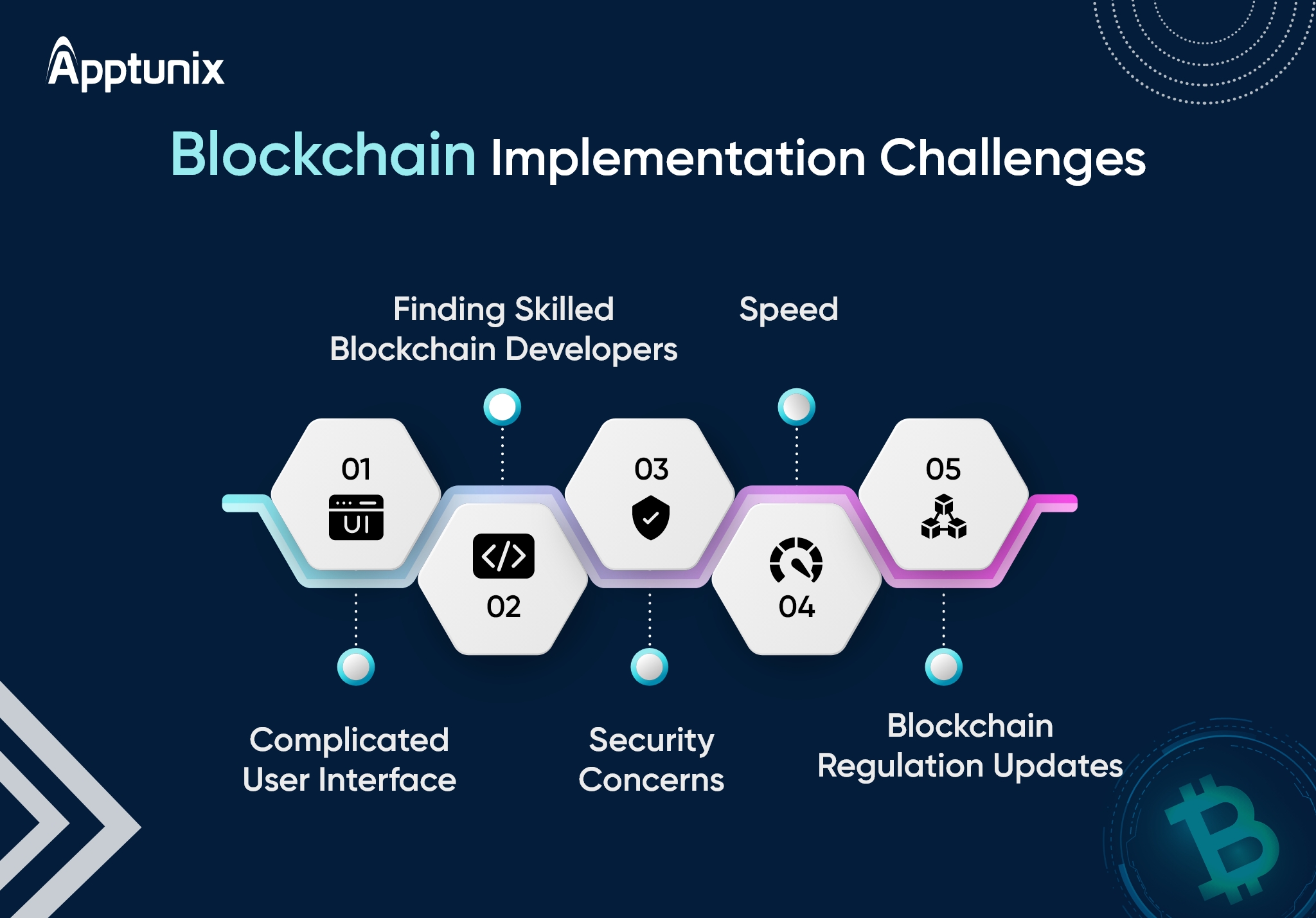

5 Blockchain Implementation Challenges to Keep in Mind

Needless to say, you are going to face a lot of challenges while implementing sophisticated blockchain technology into your business. Let’s have a look at some of the common challenges.

- Complicated User Interface

Not all of your clients may be technically sound. So keeping your system simple can be your foremost challenge. - Finding Skilled Blockchain Developers

Blockchain is one of the latest technologies so hiring skilled developers at competitive prices can be another biggest challenge. - Security Concerns

Although blockchain technology is considered safe still the 51 percent attack theory (hackers acquire about 50% of the network’s computational power) has made this technology vulnerable to threats from hackers. - Speed

Transactions Per Second (TPS) is something that is a major bottleneck hampering the mass adoption of blockchain technology. It depends upon various factors like block time, block size, transaction fees, network traffic, etc. - Blockchain Regulation Updates

The regulations often keep on changing. So it becomes difficult to consider and incorporate the regulation effect into organizations’ activities.

Also Read: Complete Guide On Blockchain App Development | Benefits & Cost Factors

Hire Blockchain Implementation Experts at Apptunix

Whatever the challenges are, blockchain technology is helping businesses across the world set new records. Whether we talk about blockchain leaders, blockchain engineers, business owners, or entrepreneurs, all are showing high interest in integrating blockchain technology.

So if you want to be a part of the trending revolution it’s the right time to dive in. What you are required to do is to hire blockchain implementation experts that can help you make a mark in the global blockchain business community.

Frequently Asked Questions(FAQs)

Q 1.Can I Build My Own Blockchain?

Yes, you can. You are free to write your own code for creating a new blockchain that is capable of supporting cryptocurrency. All it needs is extensive technical training for enhancing your coding skills and basic understanding of blockchain technology. You can also hire blockchain development company to do the job better.

Q 2.How Much Does It Cost to Build a Blockchain App?

On average, the blockchain app development cost typically ranges from $25,000 to $200,000. This cost can vary depending on the app’s complexity, the features you want, and several other factors. To get an estimated cost for your dream app you can book a free consultation.

Q 3.How Much Time Does It Take to Build a Blockchain App?

Well, for an average app, this period ranges between 3 to 6 months. It can change depending on the customization level and complexity of the app.

Q 4.Which is the Top Blockchain Platform?

Well, the list is large but Ethereum can be your choice. It is one of the oldest and most established decentralized networks. Moreover, it is less vulnerable to hacking, and power outages. There are also other options you can go with.

Rate this article!

(3 ratings, average: 4.67 out of 5)

Join 60,000+ Subscribers

Get the weekly updates on the newest brand stories, business models and technology right in your inbox.

With about 7 years of experience (Technical & SEO Writing) and a solid technical background (Master of Technology – E.C.E with Wireless Communication as specialization), he has worked both as a freelancer and on a regular basis for prestigious IT organizations across the globe. Whether it’s Blockchain, Metaverse, Artificial Intelligence (AI) & Neural Networks, Machine Learning (ML), Internet of Things (IoT), Cyber Security, Cloud Computing, 5G Technology, or some other trending technologies he has written whitepapers, eGuides, blogs, technical documentation, guest posts, and so on for almost all. Here at Apptunix, he is generating B2B content.

App Monetization Strategies: How to Make Money From an App?

Your app can draw revenue in many ways. All you need to figure out is suitable strategies that best fit your content, your audience, and your needs. This eGuide will put light on the same.

Download Now!Subscribe to Unlock

Exclusive Business

Insights!

And we will send you a FREE eBook on Mastering Business Intelligence.